Executive Summary

The fintech and digital banking sectors have witnessed extraordinary growth, with the global fintech market expanding from $194.1 billion in 2022 to an expected $492.81 billion by 2028 (Fortune Business Insights). This rapid evolution presents key challenges for traditional banks, including outdated legacy systems, regulatory pressures, and rising customer expectations for seamless digital experiences. To remain competitive, traditional financial institutions are increasingly adopting innovative technologies, collaborating with fintech startups, and enhancing their service offerings through digital transformation initiatives. By prioritizing agility, customer-centricity, and technological integration, these institutions are working to navigate the changing landscape and retain their relevance in the digital age.

Introduction

Fintech, short for "financial technology," is changing the way we think about and use money. By harnessing digital tools, software, and data-driven solutions, fintech makes financial services more efficient and accessible for everyone. This innovation has transformed traditional banking, offering faster, more user-friendly alternatives that fit our modern lifestyles. Services like mobile payments, digital lending, robo-advisors, and blockchain technology are just a few examples of how fintech is reshaping our financial landscape.

Digital banking, a vital component of fintech, enables users to access banking services effortlessly through online platforms and mobile apps. The rise of fintech truly took off after the 2008 global financial crisis. This crisis highlighted the weaknesses in traditional banking and led to a loss of trust among consumers, coupled with stricter regulations. In this climate, nimble fintech startups emerged, offering transparent, personalized, and consumer-focused financial solutions.

Digitalization has also reshaped what consumers expect from their financial institutions. Today, people want speed, convenience, and personalization in their banking experiences. A survey by Accenture and PwC found that 67% of consumers prefer digital banking to traditional face-to-face interactions. This shift is fueled by the widespread adoption of mobile technology, with 3.6 billion people expected to use mobile banking by 2024, a significant increase from 2.6 billion in 2020 (Statista, Juniper Research). The ability of fintech to deliver quick and seamless financial solutions through mobile apps, online platforms, and digital wallets has prompted traditional banks to rethink their services and adapt to this new digital-first world.

The Rise of Fintech

Overview of the Fintech Landscape

The fintech landscape is diverse and rapidly evolving, encompassing a range of services that leverage technology to improve financial offerings. Key players in this space include neobanks, which are digital-only banks providing essential banking services without physical branches, and payment platforms like PayPal and Square that facilitate digital transactions and enhance consumer payment experiences.

Additionally, robo-advisors, such as Betterment and Wealthfront, use algorithms to provide automated, low-cost investment management, making investment services more accessible to a broader audience. The fintech industry has experienced remarkable growth, with the global market expected to surge from $194.1 billion in 2022 to $492.81 billion by 2028, indicating a CAGR of 16.8%. This growth reflects increasing consumer adoption of digital solutions and the expanding role of technology in finance.

Consumer Behavior Shifts

Consumer behavior is shifting dramatically in response to the rise of fintech. Today's customers have higher expectations for banking services, emphasizing the need for convenience, speed, and personalized experiences. Digital banking allows consumers to conduct transactions anytime and anywhere, leading to a growing demand for services that cater to their on-the-go lifestyles. According to recent surveys, 67% of consumers prefer digital banking options over traditional methods, highlighting the importance of accessibility and efficiency. This shift has created a more competitive landscape, pushing traditional banks to adopt innovative solutions to meet evolving customer needs.

Regulatory Environment

The regulatory environment for fintech companies is complex and constantly evolving. Regulatory bodies are working to balance innovation with consumer protection, leading to new frameworks that govern everything from data privacy to anti-money laundering practices. Regulations such as the General Data Protection Regulation (GDPR) in Europe and the Payment Services Directive (PSD2) are shaping how fintech firms operate. These regulations not only impact fintech startups but also traditional banks, which must adapt their strategies to comply with new rules while remaining competitive. Many traditional financial institutions are responding by investing in technology to enhance compliance measures and exploring partnerships with fintech companies to stay ahead of the curve. By embracing a proactive approach to regulation, banks can better navigate this changing landscape and leverage fintech innovations to improve their service offerings.

Key Innovations Shaping Fintech

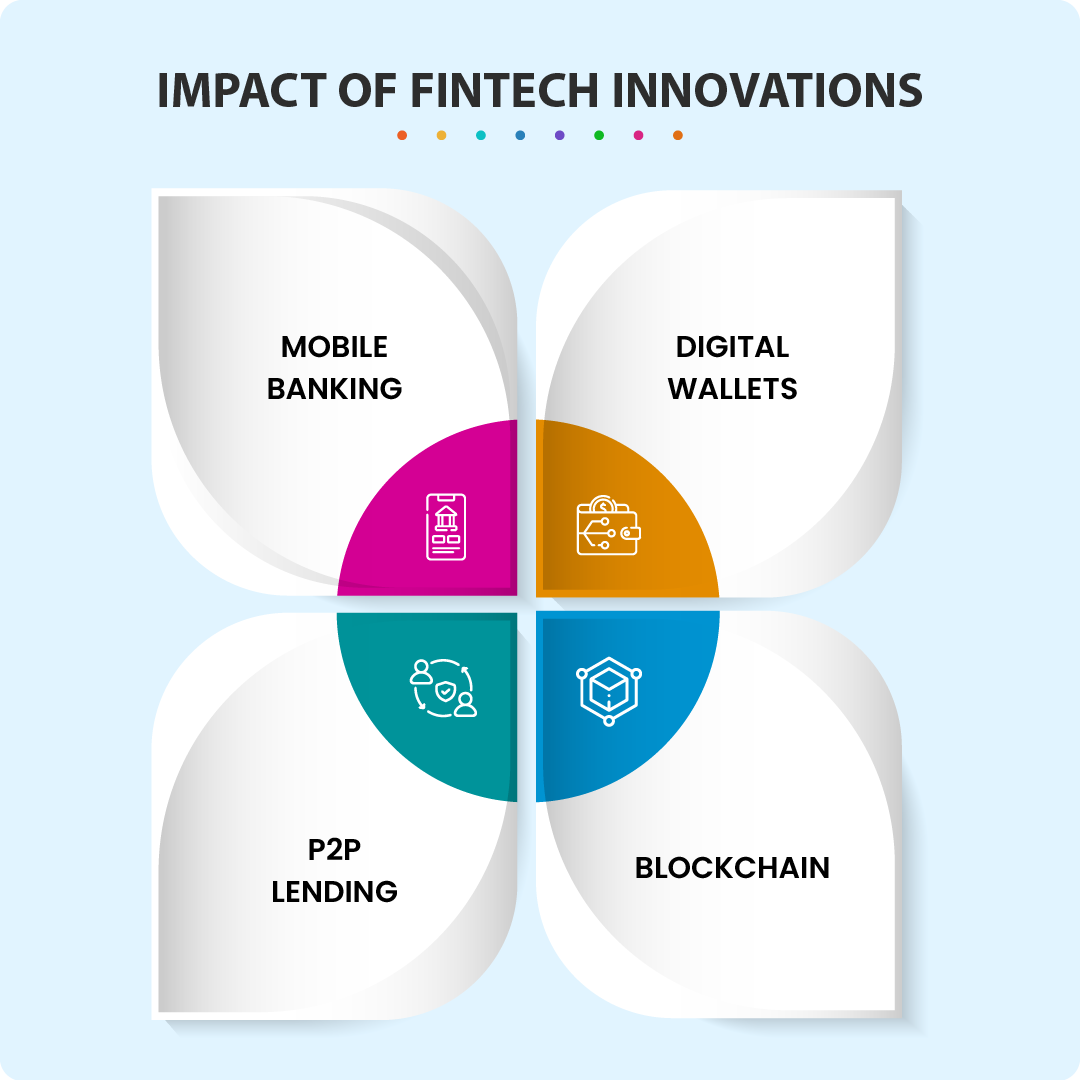

Fintech innovations have significantly transformed financial services by offering more accessible, convenient, and secure solutions. Mobile banking apps allow users to manage their finances directly from their smartphones, streamlining transactions and account management. Digital wallets, such as PayPal, Apple Pay, and Google Wallet, facilitate quick and secure digital payments, reducing reliance on physical cash and cards. Peer-to-peer (P2P) lending platforms connect borrowers with individual investors, bypassing traditional banks and providing faster approvals with potentially lower interest rates. Meanwhile, blockchain technology is enhancing security, transparency, and efficiency in financial transactions, enabling decentralized finance (DeFi) solutions where users can trade, lend, or borrow without intermediaries.

Impact of Fintech Innovations:

- Mobile banking simplifies account access and transactions, making financial management more user-friendly.

- Digital wallets promote secure, fast, and contactless payments.

- P2P lending offers a more direct and efficient way to borrow and invest money.

- Blockchain supports transparency and security, fostering the growth of decentralized financial ecosystems like DeFi.

Challenges Faced by Traditional Banks

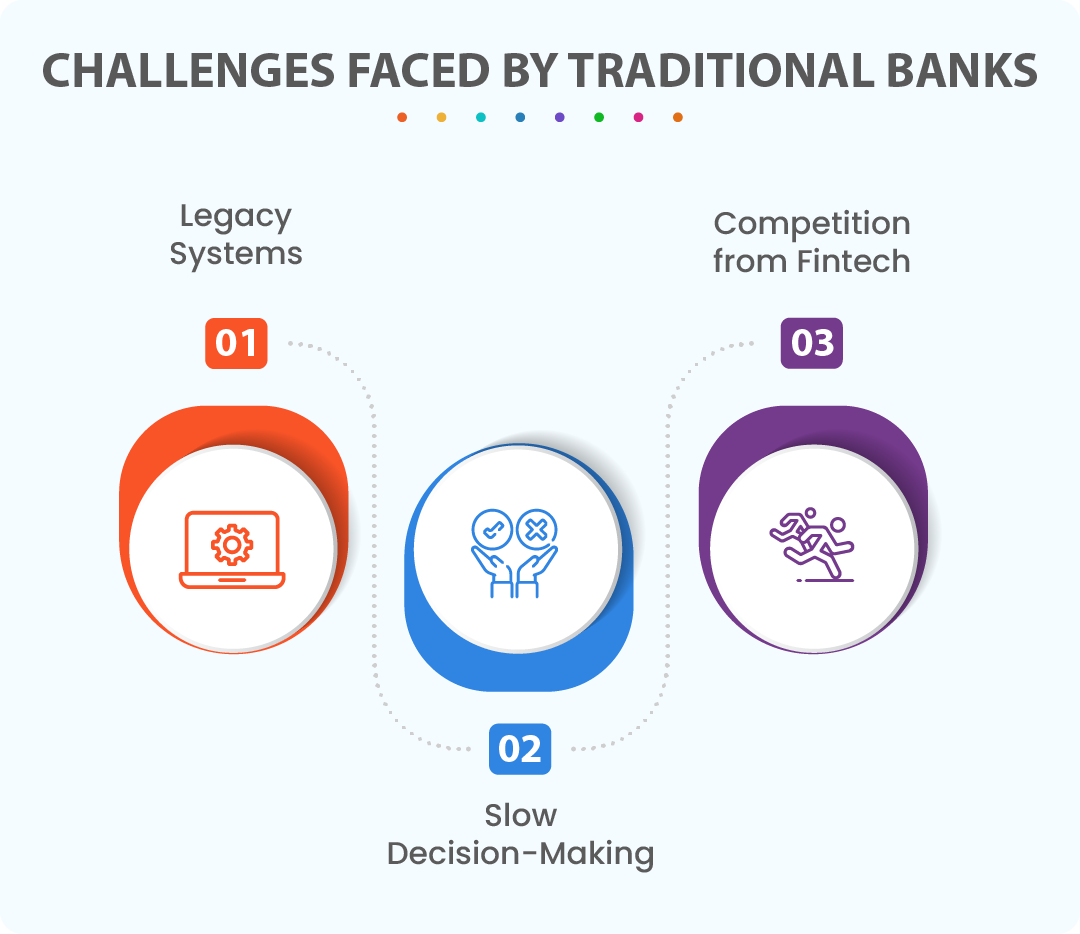

- Legacy Systems: Many traditional banks still rely on outdated technology, making it difficult to keep pace with digital innovations. These systems are costly to upgrade and lack the flexibility needed for modern banking operations.

- Slow Decision-Making: Bureaucratic structures hinder swift decision-making in traditional banks. Multiple layers of approval can slow down the adoption of new technologies and processes, making them less responsive to market demands.

- Competition from Fintech: Agile fintech companies can quickly offer innovative, customer-centric solutions, posing a significant threat to traditional banks. Their ability to operate at lower costs and provide faster, more personalized services challenges banks to keep up.

Strategies for Adaptation

As fintech continues to disrupt the financial services industry, traditional banks must adopt new strategies to remain competitive. Below are key adaptation strategies that traditional banks are implementing to thrive in the digital age:

Digital Transformation Initiatives

Traditional banks are embracing digital transformation through significant investments in cloud computing, artificial intelligence (AI), and blockchain. These technologies modernize banking infrastructure, streamline operations, and deliver more efficient services.

Cloud Computing enables banks to scale operations, enhance data storage, and improve service delivery by migrating legacy systems to the cloud. AI automates processes, enhances decision-making, and improves customer engagement through tools like chatbots and predictive analytics. AI is particularly useful in fraud detection, risk management, and offering personalized financial advice. Blockchain enhances security and transparency, with applications in faster cross-border payments and secure data sharing. Smart contracts streamline processes, eliminating intermediaries.

Collaboration with Fintech Companies

Traditional banks are increasingly recognizing the value of fintech firms, opting for strategic partnerships and acquisitions rather than viewing them as competitors. This collaborative approach allows banks to integrate innovative technologies and enhance their service offerings without developing solutions from scratch.

Strategic Partnerships involve banks teaming up with fintech companies to improve customer experiences and streamline back-end operations. These collaborations often target key areas such as payments, lending, wealth management, and digital identity verification. For instance, a bank might partner with a fintech to implement advanced payment processing systems, thus providing customers with faster and more efficient transactions.

Acquisitions offer another pathway for banks to access innovative technologies and specialized markets. By acquiring fintech firms, traditional banks can quickly incorporate cutting-edge solutions into their operations, enabling them to stay competitive in an evolving landscape. This strategy not only enhances existing services but also allows banks to enter new business segments, such as peer-to-peer lending or robo-advisory services.

Enhancing Customer Experience

In the current digital landscape, consumers demand personalized banking experiences, prompting traditional banks to leverage data analytics to meet these expectations. By analyzing customer data—including transaction history, behavior, and demographics—banks can tailor services to individual preferences. This analysis enables personalized product recommendations, targeted marketing campaigns, and proactive financial advice that align with customer needs, ultimately fostering stronger relationships and increased loyalty.

In addition to personalization, banks are prioritizing the enhancement of user interfaces across digital platforms, including mobile apps and online banking. A focus on creating intuitive, user-friendly designs is crucial for improving the overall customer experience. By simplifying interfaces and streamlining onboarding processes, banks can reduce friction and ensure seamless transactions. This emphasis on usability not only boosts customer satisfaction but also encourages more users to adopt digital banking solutions.

For example, many banks are incorporating features such as chatbots and virtual assistants into their apps, providing customers with instant support and guidance. This combination of personalized services through data analytics and improved user interfaces positions traditional banks to compete effectively in the evolving fintech landscape, ensuring they meet and exceed the growing expectations of their customers.

Innovative Product Offerings

In response to the rapid innovations in fintech, traditional banks are launching a range of new digital products, including mobile banking apps, digital wallets, and contactless payment solutions. These offerings are designed to meet the increasing consumer demand for fast, seamless, and secure digital transactions.

Mobile Banking Apps have become essential tools for customers, enabling them to manage their accounts, transfer funds, apply for loans, and even invest directly from their smartphones. Many of these apps integrate advanced security features, such as biometric authentication, ensuring that users can access their accounts securely and conveniently.

In parallel, banks are introducing Digital Wallets or partnering with existing platforms like Apple Pay and Google Pay to facilitate contactless payments. These wallets allow customers to store payment methods digitally, making secure transactions without the need for physical cards, thus enhancing convenience and efficiency in everyday transactions.

Additionally, a growing focus is on expanding services to unbanked and underbanked populations. By offering low-cost digital banking products, such as basic savings accounts, mobile money services, and micro-loans, traditional banks are tapping into new markets and promoting financial inclusion. This not only serves social needs but also represents a significant business opportunity for banks looking to grow in an increasingly competitive landscape.

Yoroflow's Role in the Fintech Ecosystem

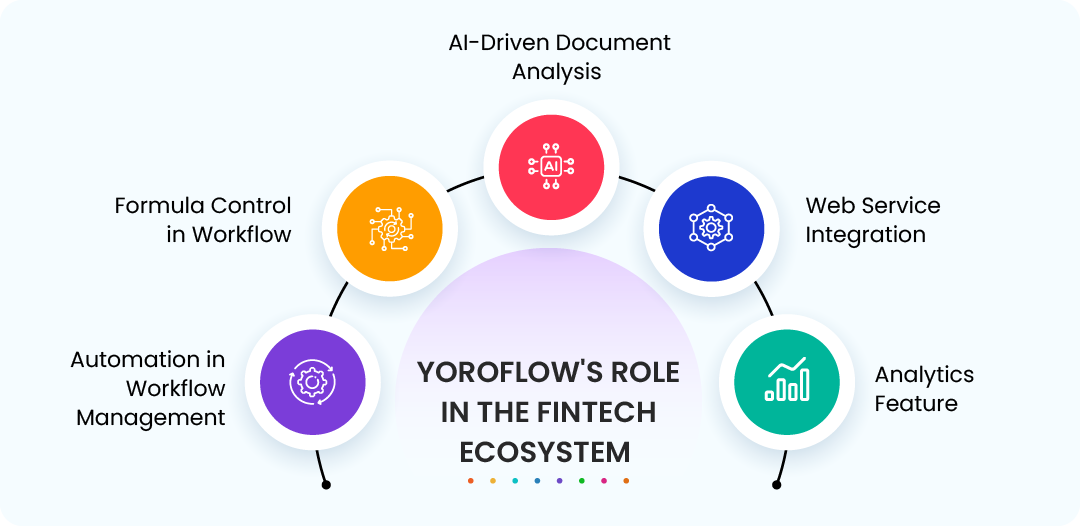

Yoroflow provides significant benefits to fintech organizations through advanced automation and intelligent workflow solutions. Here’s how Yoroflow helps specifically in fintech:

Automation in Workflow Management

Yoroflow streamlines workflow in the financial processes. The complex, repetitive processes within fintech companies by automating tasks such as loan approvals, account opening, payment processing, and compliance checks. This automation reduces manual intervention, minimizes errors, and accelerates decision-making, leading to faster service delivery and improved operational efficiency.

Formula Control in Workflow

Formula control in Yoroflow’s workflow management allows fintech companies to implement custom calculations and logic-based decision-making directly within automated workflows. This is particularly useful in scenarios like interest rate calculations, risk assessments, and financial forecasting. With formula control, workflows can automatically adjust based on dynamic financial data, improving accuracy and reducing the time spent on manual calculations.

AI-Driven Document Analysis

Yoroflow’s AI-driven document analysis automates the analysis, extraction, classification, and processing of documents such as contracts, loan applications, and compliance reports. By leveraging AI, Yoroflow can scan and interpret documents, verify information, and flag anomalies in real-time, reducing the reliance on manual review and speeding up the document processing pipeline, especially in high-volume environments.

Web Service Integration

Yoroflow’s integration with external web services allows fintech companies to link their workflows with third-party applications such as payment gateways, credit rating agencies, and identity verification services. The enhanced Web Service feature significantly improves Yoroflow’s capability to connect with various financial platforms and APIs, automating data transfers and triggering workflows based on external events. This integration creates a unified ecosystem of financial tools, enhancing efficiency and minimizing the need for manual intervention.

Analytics Feature

Yoroflow’s built-in analytics tools provide fintech firms with comprehensive insights into their operations. It provides a customizable dashboard that enables businesses to track key performance indicators (KPIs), identify bottlenecks, and optimize workflows based on real-time data. For fintech companies, this level of analytics is vital for making data-driven decisions, such as optimizing customer service, enhancing transaction security, or identifying growth opportunities.

Case Studies

As the fintech landscape evolved, several traditional banks have demonstrated remarkable adaptability by embracing innovative strategies. Here are notable examples:

JPMorgan Chase

JPMorgan Chase is leading digital transformation in banking by launching its own digital payment platform, Chase Pay and investing heavily in blockchain technology. Their JPM Coin, a digital token for instant payments between institutional clients, demonstrates their commitment to modernizing transactions. Additionally, the bank utilizes AI for fraud detection and trade execution, enhancing operational efficiency. These initiatives have streamlined services, improved customer satisfaction, and strengthened JPMorgan's competitive position in the market.

HDFC Bank

HDFC Bank is a pioneer in digital transformation within the Indian banking sector, offering a comprehensive suite of digital products, including a mobile banking app for fund transfers, bill payments, and loan applications. The bank also launched PayZapp, a platform for contactless payments and online shopping. By investing in advanced technologies like AI and machine learning, HDFC Bank has improved customer service through chatbots and personalized offerings. These initiatives have led to significant growth in customer acquisition and retention, establishing HDFC Bank as a leading private sector bank in digital banking in India.

ICICI Bank

ICICI Bank has made significant strides in adapting to the fintech landscape through its robust digital banking initiatives. The bank introduced iMobile, a comprehensive mobile banking app that offers a wide range of services, including digital loans, investment options, and payment solutions. ICICI Bank has also partnered with various fintech companies to enhance its offerings; for example, it collaborated with Paytm to provide seamless digital payment solutions. Additionally, the bank leverages AI for customer insights and risk assessment, improving operational efficiency. By focusing on digital innovation, ICICI Bank has increased its market share, improved customer satisfaction, and streamlined its services, solidifying its position as a frontrunner in the Indian banking industry.

Future Trends in Digital Banking

Predictions for the Fintech Landscape

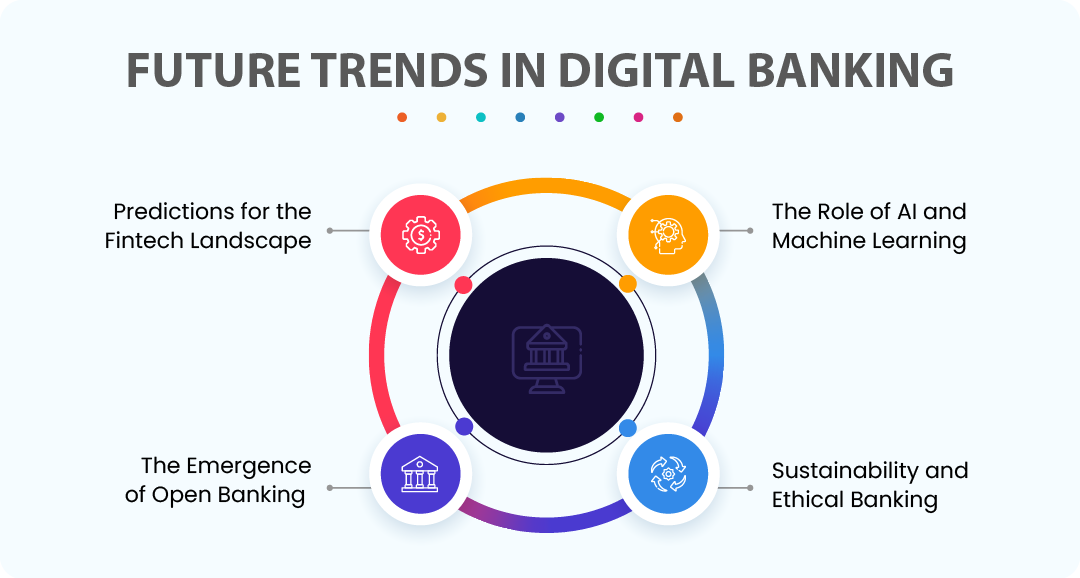

The fintech and digital banking landscape is expected to undergo significant innovations in the coming years, driven by the growing demand for convenience, personalization, and security. Embedded finance—integrating financial services into non-banking platforms—will become more common, allowing customers to access banking services within apps they use daily. Decentralized finance (DeFi) will also continue to gain traction, enabling peer-to-peer financial services through blockchain technology without traditional intermediaries. Digital currencies, such as central bank digital currencies (CBDCs), will likely emerge as mainstream payment options, reshaping how transactions occur globally. Moreover, regulatory technology (RegTech) innovations will streamline compliance, ensuring better risk management and governance across banks and fintech firms.

The Role of AI and Machine Learning

Artificial intelligence (AI) and machine learning (ML) are transforming digital banking by enhancing both customer service and decision-making. AI-powered chatbots and virtual assistants are improving customer interactions, offering 24/7 support, and resolving queries instantly. Personalization is a key trend, with AI analyzing vast amounts of customer data to provide tailored financial advice, investment suggestions, and product recommendations. In decision-making, AI and ML help banks in fraud detection, credit risk assessment, and automating routine tasks, reducing human error and operational costs. AI-driven insights also enable banks to predict customer behavior, enhancing loyalty and service innovation.

The Emergence of Open Banking

Open banking is reshaping how banks and fintech interact by allowing third-party providers to access customers' banking data (with consent) via application programming interfaces (APIs). This enables the development of innovative financial products and services tailored to customer needs, such as multi-account management tools or personalized financial dashboards. For traditional banks, open banking represents both a challenge and an opportunity. It forces them to embrace a more transparent and customer-centric approach, while also allowing fintech companies to enhance their offerings. The collaboration between banks and fintech through open banking is expected to increase competition, drive innovation, and improve customer experiences.

Sustainability and Ethical Banking

Sustainability and ethical banking are emerging as major priorities within the financial industry. Banks are increasingly focusing on green finance initiatives, such as funding renewable energy projects or offering loans with favorable terms for environmentally friendly businesses. Ethical banking practices, which emphasize social responsibility and transparency, are becoming more important to consumers, particularly millennials and Gen Z. As the demand for sustainable financial products grows, traditional banks will need to incorporate environmental, social, and governance (ESG) factors into their lending and investment strategies. Additionally, the rise of carbon-neutral banking and ethical investment funds are likely to reshape the financial sector, encouraging banks to align with global sustainability goals.

Final Thoughts

The rise of fintech has significantly transformed traditional banking, forcing established institutions to rethink their operational strategies. Fintech companies have introduced innovative technologies and business models that provide consumers with faster, more personalized services, increasing competitive pressure on banks. In response, banks are adopting strategies like digital transformation, utilizing cloud computing, artificial intelligence, and blockchain to modernize operations and improve service delivery. Additionally, many banks are forming strategic partnerships with fintech firms to integrate new technologies and expand their service offerings. By enhancing customer experience through personalized services and user-friendly interfaces, banks can better meet modern consumer expectations. Launching innovative digital products and targeting underserved markets are also essential for traditional banks to remain relevant in this evolving landscape.

In today’s rapidly evolving financial landscape, traditional banks must prioritize agility, innovation, and a customer-centric approach to remain competitive. Agility allows banks to quickly adapt to market changes and emerging trends, enabling them to seize opportunities and mitigate risks effectively. Innovation is crucial for developing new products and services that cater to the dynamic needs of consumers who demand convenience, speed, and personalization. Moreover, a strong emphasis on customer experience is essential for fostering loyalty and trust in an age where customers have countless options at their fingertips.

Yoroflow stands at the forefront of this transformation, equipping fintech companies and traditional banks with powerful tools to automate workflows and enhance operational efficiency. With seamless integration capabilities, Yoroflow allows financial institutions to connect effortlessly with external platforms, facilitating real-time data sharing and improved service delivery. By embracing these principles and leveraging solutions like Yoroflow, traditional banks can effectively navigate the challenges posed by fintech and thrive in the future of banking.